Canada · CAD · 2026 rules

The Cheque That Made Me Stop and Stare

I remember sitting at my kitchen table in Moncton on a grey January morning, my coffee going cold beside me, staring at my first CPP direct deposit notice from Service Canada. The figure was $1,433 — the maximum CPP retirement benefit at age 65 in 2026. I’d been expecting something close to that, but what I hadn’t fully anticipated was the separate line item that explained why my benefit was sitting at the top of the range. Buried in the calculation was a credit I almost scrolled past: the CPP enhancement, built up over seven years of contributions, had added roughly $84 per month to my base amount. For someone who spent three decades as a registered nurse at the Moncton hospital, that extra $84 wasn’t pocket change — it was a grocery run, a utility bill, a small but real piece of my dignity in retirement.

My name is Linda Tremblay, and I want to walk you through exactly what happened, because I’ve spoken to friends in Fredericton and Dieppe who had no idea this enhancement even existed. If you’re 50-plus and still contributing to CPP, or if you’re about to draw your pension, this story is for you.

What the CPP Enhancement Actually Is — and Why 2026 Is a Turning Point

The CPP enhancement is a federal reform that began phasing in back in 2019. The goal was straightforward: lift CPP’s income replacement rate from 25% of pensionable earnings up to 33%. That doesn’t sound dramatic until you do the math on a full career. For workers like me who contributed through the entire ramp-up, the difference compounds meaningfully by the time the first cheque arrives.

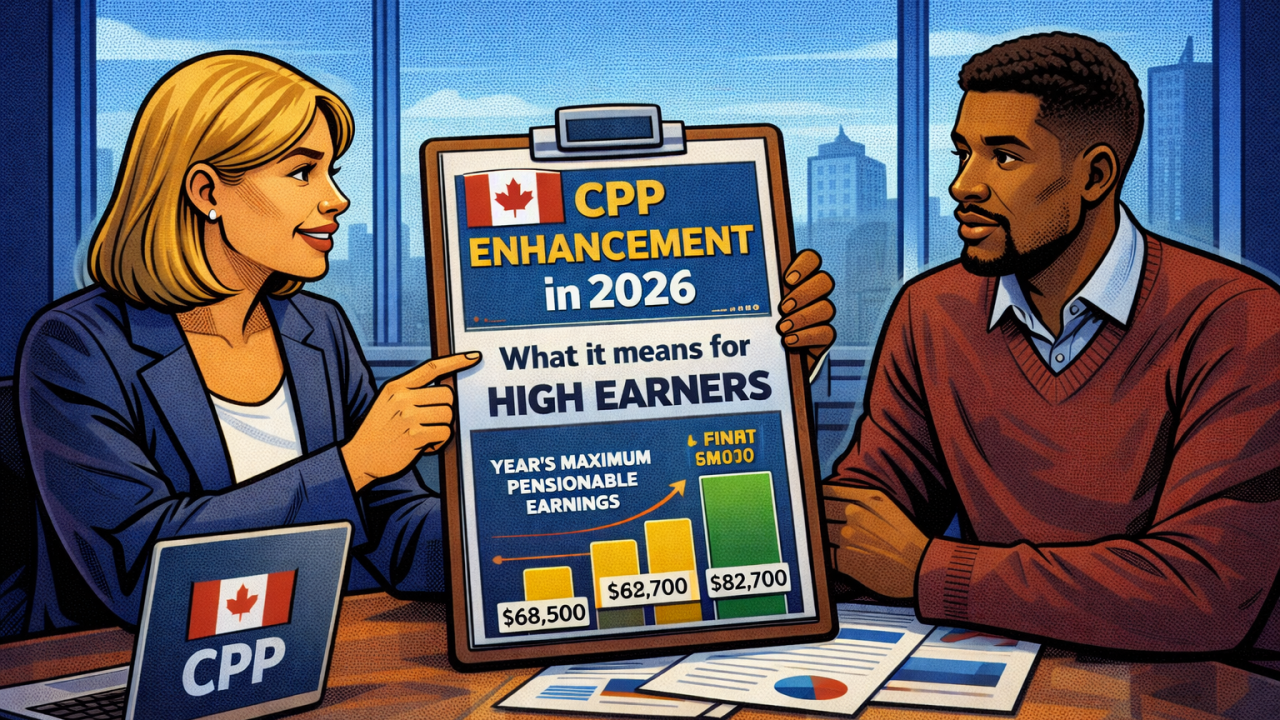

Here’s the piece that tripped me up initially. The enhancement has two layers. The first layer — what the CRA calls CPP1 — covers earnings up to the Year’s Maximum Pensionable Earnings, which sits at $71,300 in 2026. The contribution rate on that band is 5.95% from the employee and 5.95% from the employer, for a combined 11.90% if you’re self-employed. That part most people have heard of.

“

Over a 20-year retirement, that $84-per-month difference is more than $20,000 in additional income — before any future indexing. It’s the kind of number that doesn’t feel real until you write it down.— Linda

But there’s a second layer, called CPP2, that almost nobody was talking about at the nurses’ station when I was still working. CPP2 covers earnings between the YMPE and a higher ceiling called the Year’s Additional Maximum Pensionable Earnings — the YAMPE. In 2026, that YAMPE sits at approximately $82,700. So if you earned anywhere between $71,300 and $82,700 in recent years, you and your employer each contributed an additional 4% on that band. For Linda, who was earning above the YMPE for most of her final working years in New Brunswick, that second tier of contributions has been quietly stacking up since 2024.

In 2026, we are in Year 7 of the 10-year ramp. The enhancement isn’t fully baked yet — that happens closer to 2034 for workers who contribute from start to finish — but for those of us drawing CPP now, we’re already receiving a meaningfully larger benefit than retirees who left the workforce before 2019.

What Linda Actually Did — and When She Did It

On 14 October 2025, I logged into my My Service Canada Account and formally applied for my CPP retirement pension to begin in January 2026. I chose 65 precisely — not early at 60, not deferred to 70 — because my financial situation, my health, and the numbers all pointed to starting on time. The Service Canada online tool showed me a projected benefit based on my Statement of Contributions, and I could see both the base CPP component and the enhanced component listed separately.

What I did next made a real difference: I called Service Canada’s general line and asked a specific question. I wanted to confirm that my CPP2 contributions from 2024 and 2025 — those earnings between the YMPE and the YAMPE — were captured in my benefit calculation. The agent confirmed they were, and explained that the enhanced portion is calculated on a separate notional account within CPP. Because I had contributed at the 4% CPP2 rate on earnings above $68,500 (the 2024 YMPE) and above the 2025 YMPE, those contributions generated additional entitlement on top of my base CPP.

Log into My Service Canada Account and download your Statement of Contributions — look for CPP2 contributions from 2024 and 2025 on earnings above $71,300. *

Confirm your projected CPP benefit amount; the 2026 maximum at age 65 is $1,433/month — know where you stand relative to that ceiling. *

Apply for CPP (and OAS if eligible) at least 6 months before your intended start date to avoid payment delays. *

Estimate your total net income on Line 23500 of your T1 — if it approaches $93,454, model how RRIF withdrawals or investment income could affect your OAS. *

Check your available TFSA room (up to $102,000 cumulative in 2026) and consider moving income-generating assets inside the TFSA to protect OAS.

If you have a lower-income spouse, review Form T1032 for pension income splitting — up to 50% of eligible pension income can be allocated to reduce your household tax bill.

Linda also made a point of checking her CRA My Account in early February 2026 to verify the T4A(P) slip that Service Canada issues for CPP income. The slip confirmed the full $1,433 monthly amount — the maximum CPP retirement benefit for a 65-year-old in 2026 — and I filed that figure on my 2025 T1 return, which was due by 30 April 2026.

One more thing I did: I enrolled in OAS at the same time. The maximum OAS pension for ages 65 to 74 in 2026 is approximately $727 per month, indexed quarterly. Combined with CPP, that gave me a base of roughly $2,160 per month in public pension income before any RRIF withdrawals. Not a fortune, but a solid floor — and far more than I would have received had I retired before the enhancement began.

How the Numbers Stack Up — and What You Should Watch

Let me be specific, because vague reassurance doesn’t pay bills. The CPP enhancement, at full phase-in, will replace 33% of covered pensionable earnings. We’re not there yet in 2026 — Year 7 of 10 — but the trajectory is clear. For workers who contributed through the full ramp, the enhancement adds a meaningful layer on top of the base 25% replacement rate that existed before 2019.

For Linda, the rough math works like this. My base CPP entitlement, built on decades of contributions before the enhancement began, was already near the maximum. The enhancement topped it up. That $84-per-month difference I mentioned at the start? Over a 20-year retirement, that’s more than $20,000 in additional income — before any future indexing. It’s the kind of number that doesn’t feel real until you write it down.

There are a few things I’d flag for anyone in a similar position across Canada — whether you’re in Ontario, British Columbia, or right here in New Brunswick:

- Check your Statement of Contributions. You can access it through My Service Canada Account. Look for contributions made after 2019, and specifically after 2024 when CPP2 kicked in. If you earned above the YMPE in those years, you should see CPP2 contributions listed.

- OAS clawback threshold matters. If your net income on Line 23500 of your T1 exceeds $93,454 (based on 2025 income), the CRA begins recovering OAS at 15 cents per dollar above that threshold. My combined income stayed well below that, but it’s worth knowing where the line sits.

- TFSA room is still available. The 2026 annual TFSA contribution limit is $7,000, and if you’ve never contributed, cumulative room since 2009 is approximately $102,000. Sheltering investment income inside a TFSA keeps it off Line 23500 and protects your OAS.

- RRIF timing is fixed by law. If you still have an RRSP, the CRA requires it to be converted to a RRIF by the end of the year you turn 71. At age 72, the minimum annual withdrawal factor is 5.40%. Plan ahead so mandatory withdrawals don’t push you unexpectedly toward the OAS clawback zone.

- Pension income splitting is real money. If you have a lower-income spouse, you can allocate up to 50% of eligible pension income — including RRIF withdrawals — to them using Form T1032. This can reduce your combined household tax bill significantly.

Linda spent an afternoon in late November 2025 running these numbers with a pencil and a printed CRA worksheet. No apps, no guesswork — just the actual figures from my Service Canada statement and my RRSP balance. It took about two hours and gave me more confidence than anything else I did in my retirement preparation.

Show the math: How Linda’s Enhanced CPP Was Calculated

What This Means for the Next Generation of Retirees

Here’s the bigger picture. The CPP enhancement was designed for workers who are 40 or 50 today — people who have decades of enhanced contributions ahead of them. By the time the ramp completes around 2034, workers who contributed through the full 10-year phase-in will retire with a CPP that replaces a full third of their covered earnings, up from a quarter. That’s a structural improvement in Canada’s retirement system, and it’s funded by the contributions you and your employer are making right now.

For Linda, drawing CPP in January 2026, the benefit is partial — I caught the tail end of the ramp, not the full ride. But even a partial enhancement, compounded over a full career of contributions near the YMPE and YAMPE ceilings, produced that $84-per-month difference I almost missed. Imagine what it will mean for a 45-year-old nurse in Regina or a 38-year-old tradesperson in Calgary who contributes at the enhanced rate for the next 25 years.

The system isn’t perfect. The enhancement doesn’t help workers who spent their careers below the YMPE, and the CPP2 band between $71,300 and $82,700 only benefits higher earners. GIS recipients — those relying on the maximum single benefit of approximately $1,087 per month — often see little direct gain from CPP enhancement because GIS is income-tested. These are real limitations worth acknowledging.

But for the middle-income workers who contributed steadily, who showed up to work in hospitals and schools and warehouses across New Brunswick and every other province, the enhancement is doing exactly what it was designed to do. My first cheque proved it.

If you’re approaching 65 and haven’t yet reviewed your Statement of Contributions on My Service Canada Account, do it this week. Not next month. This week. The numbers are there, they’re yours, and — as I learned on a cold January morning in Moncton — they might be higher than you think.

Frequently Asked Questions

Last reviewed: April 2026. Figures reflect 2026 rules and are not financial advice.

Leave a Reply