If you are thinking about when to claim Social Security, July 2026 is a good moment to pause and look at the full picture. Your payment date, your monthly amount, and the age you choose to start all work together. This guide walks you through each piece so you can make a confident choice.

How the July 2026 Payment Schedule Works

Social Security retirement and disability payments go out on Wednesdays. Which Wednesday depends on your birthday.

If your birthday falls on the 1st through the 10th, your payment arrives on the second Wednesday of the month.

If your birthday falls on the 11th through the 20th, your payment arrives on the third Wednesday of the month.

If your birthday falls on the 21st through the 31st, your payment arrives on the fourth Wednesday of the month.

There is one important exception. If you started receiving Social Security before May 1997, or if you receive both Social Security and SSI, your payment comes on the first Wednesday of the month instead. The same rule applied in June 2026, when that group was paid on Wednesday, June 3, 2026.

You can always confirm your exact July date at SSA.gov’s official 2026 payment calendar. Payments go directly to your bank or Direct Express card on the scheduled day.

SSI payments follow a different rhythm. SSI is paid on the first of each month. When the first falls on a weekend or holiday, SSI pays early. Always check the SSA calendar to be sure.

Why Your Claim Age Changes Everything

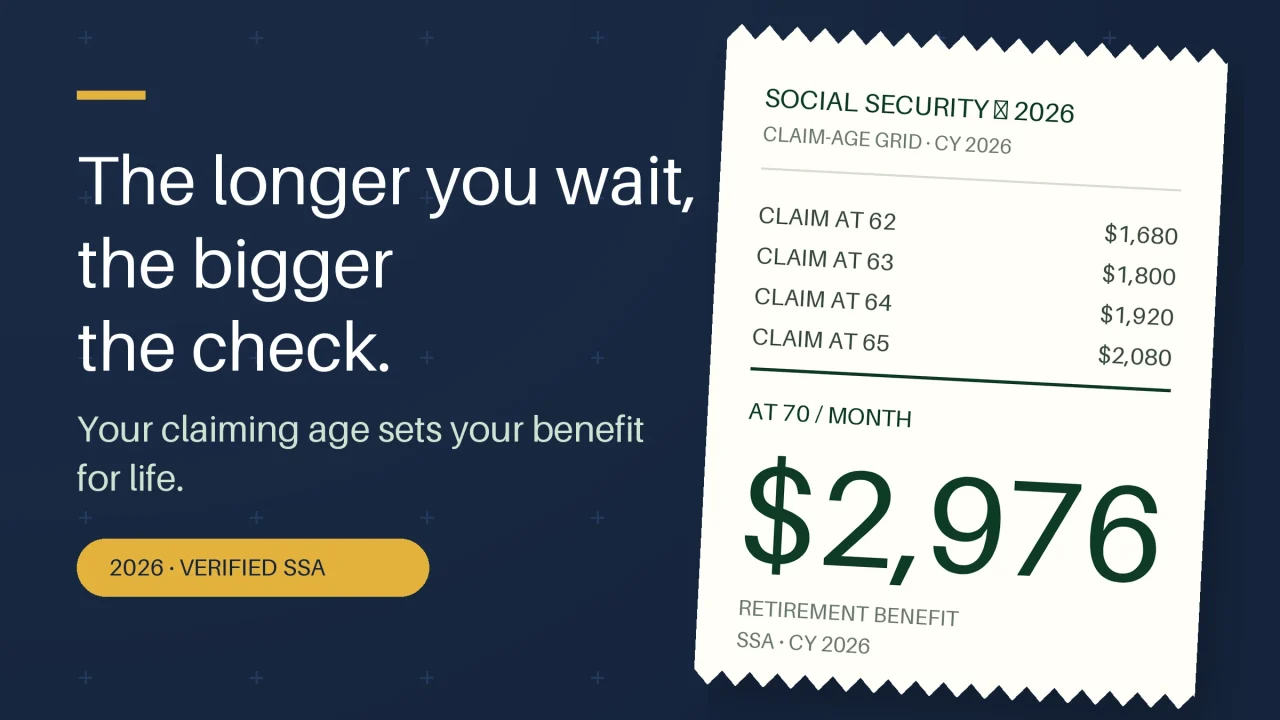

The age you choose to start benefits is the single biggest factor in your monthly amount. Social Security lets you claim as early as age 62 or as late as age 70. Every year you wait, your monthly check grows.

The example below uses a worker with a full retirement age benefit of $2,400 per month. Claiming at 62 drops that to $1,680 per month. Waiting until 70 raises it to $2,976 per month. That difference between the earliest and latest ages is meaningful for every month of retirement.

Waiting also helps a surviving spouse. The survivor benefit floor matches what you were receiving. A higher benefit while you are alive means a higher floor for your spouse after you are gone.

Claiming at 62 yields $1,680 per month, while waiting until 70 produces $2,976 per month — and the survivor benefit floor matches whichever amount you were receiving.

The Crossover Point

Claiming early means more checks, but smaller ones. Claiming later means fewer checks, but larger ones. At some point, the total dollars received by a later claimer catches up to and passes the total received by an earlier claimer. That point is called the crossover age, sometimes called the break-even age.

For this example, the crossover age is 80.37. If you live past that age, waiting to claim produces more total income. If you have reason to expect a shorter life, claiming earlier may make more sense for you personally.

The chart below shows how lifetime totals build up over time at each claiming age.

The crossover age for this example is 80.37 — the point at which a later claimer’s total lifetime benefit surpasses an earlier claimer’s.

Working While Collecting

Many people want to keep working after they start benefits. That is allowed, but there are limits if you have not yet reached your full retirement age.

In 2026, if you are under full retirement age for the whole year, Social Security withholds $1 for every $2 you earn above $24,480 per year. In the year you reach full retirement age, the limit rises to $65,160 per year, and the withholding rate drops to $1 for every $3 over the limit.

Once you reach full retirement age, the earnings test goes away completely. You can earn any amount without any reduction to your benefit.

The example below shows what happens if you earn $35,000 in a year while collecting early. Social Security would withhold $5,260, leaving you with $29,740 in net earnings after the offset. The withheld amount is not lost forever — SSA recalculates your benefit upward once you reach full retirement age.

On $35,000 of earnings, Social Security withholds $5,260, leaving $29,740 in net earnings after the offset.

Taxes on Your Benefit

Social Security benefits may be partly taxable at the federal level. The amount that is taxable depends on your “combined income,” which is your adjusted gross income plus nontaxable interest plus half of your Social Security benefit.

For single filers, up to 50% of benefits may be taxable if combined income is between $25,000 and $34,000. Above $34,000, up to 85% may be taxable.

For joint filers, the 50% range runs from $32,000 to $44,000. Above $44,000, up to 85% may be taxable.

In this example, the provisional income is $41,600. That puts a single filer in the up-to-50% band. The widget below shows exactly where your income lands.

With provisional income of $41,600, up to 50% of benefits may be subject to federal income tax.

Other Programs You May Qualify For

Social Security is often just one piece of a larger support picture. Depending on your income and resources, you may also qualify for help with Medicare costs, prescription drugs, food, or energy bills.

The eligibility screen below checks several programs based on your income level. In this example, the household income is about 113% of the federal poverty level. The 2026 poverty guideline for a two-person household is $21,640 per year.

Programs like Extra Help for prescriptions and SNAP for food assistance may be available even to people with moderate incomes. It is always worth checking.

At 113% of the federal poverty level, this household is likely eligible for programs including Extra Help for prescriptions, SNAP, and LIHEAP energy assistance.

The 2026 Cost-of-Living Adjustment

Benefits received in July 2026 already include the 2026 cost-of-living adjustment. SSA applied a 2.8% increase effective January 2026. That adjustment went to about 71 million beneficiaries. SSI recipients saw their increase effective December 31, 2025.

The 2026 SSI federal benefit rate is $994 per month for an individual and $1,491 per month for a couple. These amounts reflect the 2.8% adjustment.

Recent Changes That May Affect Your Payment

The Social Security Fairness Act was signed on January 5, 2025. It repealed two rules — the Windfall Elimination Provision and the Government Pension Offset — for benefits payable after December 2023. SSA sent about $17 billion in retroactive payments to roughly 3.1 million beneficiaries by July 2025. If you worked in a job not covered by Social Security, such as certain government or teaching positions, this change may have increased your benefit.

A separate April 2026 audit by the SSA Office of Inspector General found that 8,618 widow and widower beneficiaries had been underpaid. The total underpayment was $50.4 million. If you are a surviving spouse, it is worth contacting SSA to confirm your payment is correct.

If SSA ever notifies you of an overpayment, you have 60 days from the notice to file a Request for Reconsideration using Form SSA-561. A waiver request using Form SSA-632 has no time limit. For Title II benefits, the default recovery rate was reinstated to 100% of the monthly benefit for overpayments occurring after March 27, 2025. For SSI, the recovery rate is 10% of the monthly payment. You can request a lower rate at any time.

If You Have a Defaulted Student Loan

If you have a defaulted federal student loan, the Treasury can offset your Social Security benefit. The offset is capped at 15% of your monthly benefit. However, the law protects a floor of $750 per month — no offset can reduce your payment below that amount.

Survivor and Death Benefits

When a Social Security recipient dies, an eligible surviving spouse or child can apply for a one-time lump-sum death payment of $255. You apply using Form SSA-8 and must do so within two years of the death.

Survivor benefits are an important reason to think carefully about your claiming age. The benefit your surviving spouse receives is tied to what you were collecting. Delaying your own claim can leave a larger financial foundation for a spouse who outlives you.

How to Reach SSA

You can call SSA’s national line at 1-800-772-1213, Monday through Friday. If you are deaf or hard of hearing, the TTY line is 1-800-325-0778. You can also visit your local SSA office or manage many tasks online at SSA.gov.

If you want to apply, update your direct deposit, or check your payment status, the online my Social Security portal is often the fastest option. For complex questions about your specific situation — especially if you are a widow or widower, a government employee, or someone with a disability — a phone call or in-person visit is worth the time.

Putting It All Together

Your July 2026 payment date is set by your birthday and the Wednesday schedule. Your monthly amount is set by the age you chose to claim. And the programs available to you depend on your total income picture.

Understanding all three pieces together gives you the clearest view of what Social Security means for your household. Use the tools in this guide as a starting point, then confirm your details directly with SSA before making any final decisions.

Leave a Reply