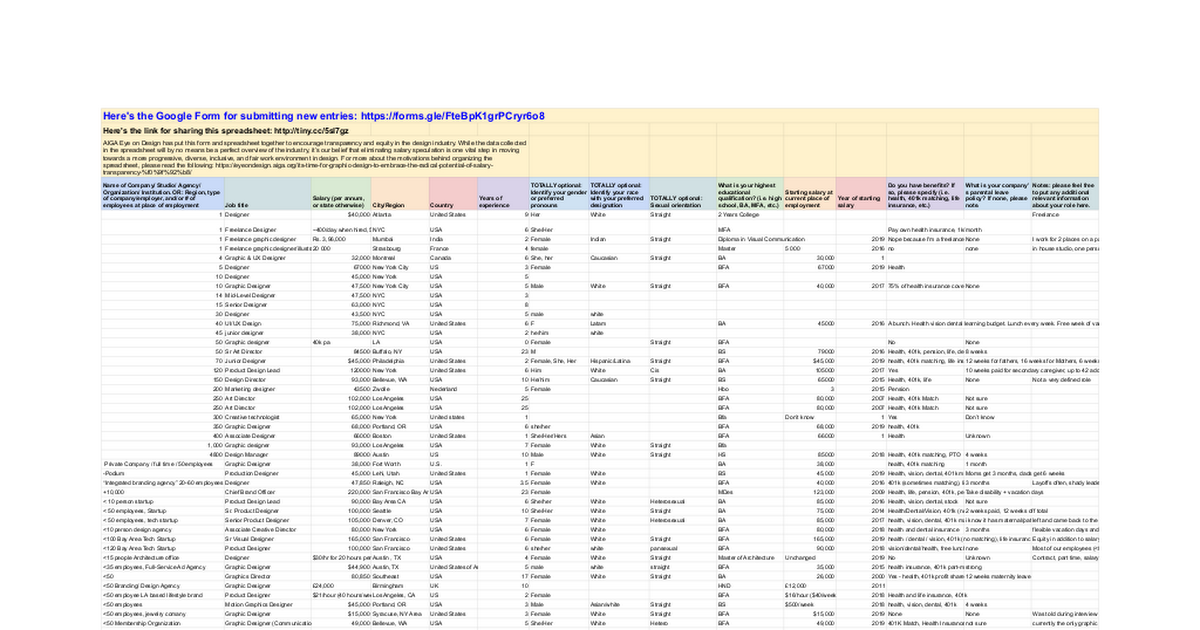

A family earning $75,000 in San Francisco, California needs just $41,000 to maintain the same lifestyle in Tulsa, Oklahoma — a difference of roughly $34,000 per year, untouched. That’s not a rounding error. That’s a second income. Understanding exactly how that number gets calculated is the difference between a move that transforms your finances and one that simply relocates your stress.

The cost of living index compares expenses across cities using housing, food, education, healthcare, transportation, and taxes as its core inputs. Knowing which of those inputs drives your personal budget — not just the composite score — is what actually makes relocation math work in your favor.

Why the Migration Maps Are Pointing Toward Mid-Size Cities

Read more: Cheapest States to Live in America

The post-pandemic migration story hardened into a recognizable pattern by . Coastal metros shed residents. The Sun Belt absorbed them. Then the Sun Belt got expensive too. Austin, Texas — once the poster child for affordable relocation — now sits above the national average on most composite indexes, with median 1-bedroom rents hitting $1,680/month as of early .

The new migration edge belongs to overlooked metros: Knoxville, Tennessee. Columbus, Ohio. Huntsville, Alabama. Spokane, Washington. These cities score between 85 and 95 on the Council for Community and Economic Research (C2ER) composite index — meaning everyday costs run 5 to 15 percent below the U.S. baseline of 100.

COL Index (U.S.=100)

COL Index (U.S.=100)

Phoenix, AZ (2026)

Knoxville, TN (2026)

How the Cost of Living Index Is Actually Built

The C2ER index — the most widely used benchmark — assigns weights to six spending categories based on average American household allocation. Housing carries the heaviest load, accounting for roughly 30 percent of the composite score. That’s why two cities can have nearly identical grocery prices but wildly different index scores.

The factors are housing, food, education, healthcare, transportation, and taxes — each one a variable you can actually audit for your specific situation. A remote worker with no commute, for example, can functionally ignore the transportation component. A family with two kids in private school should weight education far above the index’s average assumption.

Here’s a practical breakdown using Huntsville, Alabama (COL index: ~87) versus Denver, Colorado (COL index: ~114) for a hypothetical household spending $5,500/month:

| Expense Category | Huntsville, AL | Denver, CO | Annual Gap |

|---|---|---|---|

| Housing (3BR home) | $1,350/mo | $2,640/mo | $15,480 |

| Groceries (family of 4) | $820/mo | $1,010/mo | $2,280 |

| Healthcare (premiums) | $540/mo | $690/mo | $1,800 |

| Transportation | $480/mo | $620/mo | $1,680 |

| Total Annual Savings | — | — | ~$21,240 |

Remote Work Viability and the Job Market beneath the Index

A low COL score is almost meaningless if the local job market can’t support you. Madison County, Alabama — home to Huntsville — is an instructive exception. The Redstone Arsenal and NASA Marshall Space Flight Center anchor a defense and aerospace corridor that employs over 40,000 people. Median household income in the county runs roughly $72,000, above the national median.

For remote workers, the calculus is simpler but still requires scrutiny. Budgeting starts with your after-tax income — not gross salary. A $110,000 remote salary earned in Nashville, Tennessee (no state income tax) versus the same salary earned while living in Portland, Oregon (9.9% top marginal rate) is a difference of over $7,000 per year in take-home pay, before touching cost-of-living differences at all.

Cost of living indexes can make cheap cities look like bargains — but they don’t measure misery. Jackson, Mississippi ranks among the cheapest metros in America. It also has among the highest violent crime rates, crumbling water infrastructure, and a median household income of just $41,000. Low cost and low quality are not the same thing.

What the Indexes Quietly Leave Out

Standard COL indexes track prices. They don’t track quality. Two cities can have identical grocery scores while one has a thriving farmers market scene and the other has a single aging supermarket with sparse shelves. The number looks the same. The experience isn’t.

Healthcare is the starkest example. The Kaiser Family Foundation tracks insurance premiums by state. A 55-year-old buying a benchmark silver plan in Lubbock, Texas pays roughly $612/month before subsidies. The same plan in Hartford, Connecticut runs closer to $820/month. That’s a $2,496 annual gap — rarely reflected in headline COL comparisons.

Property taxes are equally distorting. Naperville, Illinois sits in DuPage County, which carries effective property tax rates above 2.1%. A $350,000 home there costs over $7,350 annually in taxes. A comparable home in Huntsville, Alabama — with a 0.41% effective rate — costs under $1,435. That’s nearly $500/month in real purchasing power, invisible in most COL calculators.

Effective property tax rate, DuPage County, IL

Effective property tax rate, Madison County, AL

Annual savings on a $350K home by moving south

Commute cost is another ghost expense. The Bureau of Labor Statistics estimates Americans spend an average of $10,961 annually on vehicle transportation. If relocating to a walkable city like Hoboken, New Jersey eliminates a second car entirely, that’s a real cost-of-living drop that no index captures automatically.

How to Build Your Own Honest Cost Comparison

Generic indexes are a starting point — not a verdict. A rigorous personal comparison requires five layers of real math.

Use your destination state’s actual marginal rate. The Tax Foundation publishes current state income tax tables. Don’t forget local city taxes — New York City levies an additional 3.876% on top of state.

Pull active listings on Zillow or Redfin for your target ZIP code. Compare 30-year mortgage payments at current rates — not COL index “housing scores.” Factor in HOA fees and flood insurance if applicable.

County assessor websites are public. Travis County, Texas posts effective rates online. Don’t assume Texas is cheap because it has no income tax — Austin‘s property taxes routinely exceed those in states people flee.

Use healthcare.gov‘s plan comparison tool for your target state and ZIP. Premiums vary by county — not just state. Palm Beach County, Florida and Duval County, Florida can differ by $150/month for identical plan tiers.

Is your destination car-dependent? Add insurance, fuel, and maintenance. Detroit, Michigan has some of the highest auto insurance rates in the country — averaging over $4,788/year according to ICIR. That’s a cost-of-living factor most calculators ignore entirely.

The Question COL Indexes Can’t Answer

In , the U.S. Census Bureau reported that Boise, Idaho had one of the fastest-growing populations in the nation. People fled expensive coastal metros for what appeared — on paper — to be a dramatically cheaper city. By , Boise’s median home price had nearly doubled from pre-pandemic levels. The arbitrage window closed fast.

COL indexes are backward-looking snapshots. They capture what prices were when the data was collected. A city with strong job growth, a booming tech scene, or significant migration inflows — like Chattanooga, Tennessee has experienced — may look cheap in the index today but be measurably more expensive within 18 months of your arrival.

The better question isn’t “Is this city cheap?” It’s “Will this city remain affordable on my specific income, with my specific spending habits, and at the pace it’s currently growing?” That requires reading local planning commission reports, tracking rental vacancy rates from the Census Housing Vacancy Survey, and understanding whether that low sticker price reflects genuine value or decades of disinvestment.

“Cheap” is a moment in time. Affordable is a structural condition.

The difference determines whether your move

Frequently Asked Questions

You Might Also Like

I Tracked $994 in SSI Across Rural America — The Gap Is Shocking

$994/month is the 2026 SSI federal benefit rate after a 2.8% COLA — but in…

I Priced My Denver Life in Tulsa — Saved $10,440 in Year One

Oklahoma's 2026 COL index hits 85.5 — the cheapest in America. A $6K/month Denver lifestyle…

Galena Housing Drops 62% in 2026 — Before Illinois Taxes Hit

Galena's $206K median home price attracts retirees, but Illinois taxes and limited healthcare create budget…

Leave a Reply